The $16,000 Miss That Triggered a $1 Million Bill

A landlord's liquidated-damages clause turned one late payment into a million-dollar demand — until New York's top court called it a penalty

What happened

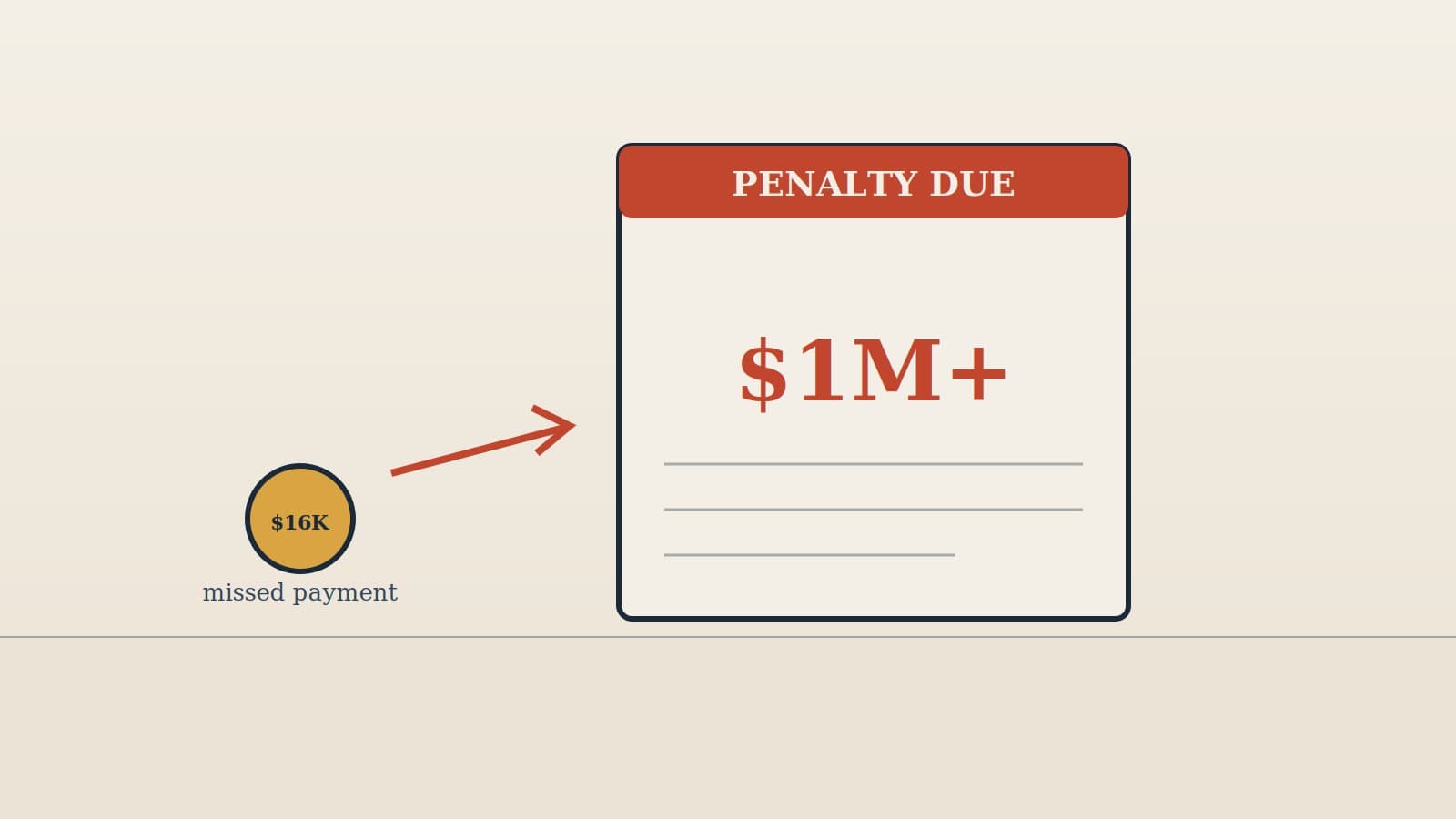

D'Agostino Supermarkets had a commercial lease with the Trustees of Columbia University. To resolve a dispute, the parties signed a surrender agreement under which D'Agostino would make a series of installment payments. D'Agostino paid the large majority of what it owed, then failed to make the final monthly payment — roughly $16,000.

Under the agreement's liquidated-damages clause, Columbia argued that this default entitled it to accelerate and collect a sum exceeding $1 million, plus interest and costs.

The trap in the contract

The clause was structured so that a relatively small breach near the end of performance unlocked an enormous, fixed payment. As the court illustrated with a simple hypothetical: a tenant who timely made all but the very last surrender payment of about $16,000 could be held liable for over $1 million — even though the actual harm from missing that last payment was, at most, the unpaid amount plus interest.

That gap between actual loss (~$16,000 + interest) and demanded damages (>$1 million) is the hallmark of a penalty. Under New York law, a liquidated-damages clause is unenforceable when:

- the actual damages were readily ascertainable at the time of contracting, or

- the stipulated amount is "conspicuously disproportionate" to the probable or actual loss.

Here, the loss from a missed installment was easy to measure and the clause's amount dwarfed it.

What the court did

The New York Court of Appeals — the state's highest court — held the liquidated-damages provision an unenforceable penalty. Columbia could recover its actual damages (the unpaid amount due plus interest), but not the grossly inflated sum the clause purported to impose. The court reaffirmed that a provision requiring damages "grossly disproportionate" to the actual loss exists to compel performance through fear of the disproportion itself — which the law won't enforce.

Why this matters for predatory contracts today

This principle protects people far beyond commercial leases. It applies to settlement agreements, service contracts, construction deals, and consumer agreements that bury oversized "default" or "acceleration" charges:

- A California example: in Greentree Financial Group v. Executive Sports, a $45,000 stipulated judgment on a $20,000 settlement was struck as an unenforceable penalty because it bore no reasonable relationship to anticipated damages.

- Courts generally allow some cushion (a landlord recovering two-to-three times existing rent has been upheld), but multiples like 7½ times estimated damages have been rejected as penalties.

Red flags to check your own contract for

- A fixed "default" charge far larger than the harm a breach would actually cause.

- Acceleration clauses that make a small missed payment trigger the entire balance plus extras.

- A flat penalty that ignores how much you'd already performed (paying 95% doesn't reduce it).

- Damages that are easy to calculate yet replaced by a much bigger fixed number.

- Language clearly meant to scare you into compliance rather than estimate real loss.

This article is general legal information, not legal advice. The line between enforceable liquidated damages and an unenforceable penalty is fact-specific and varies by state. Consult a licensed attorney about your agreement.