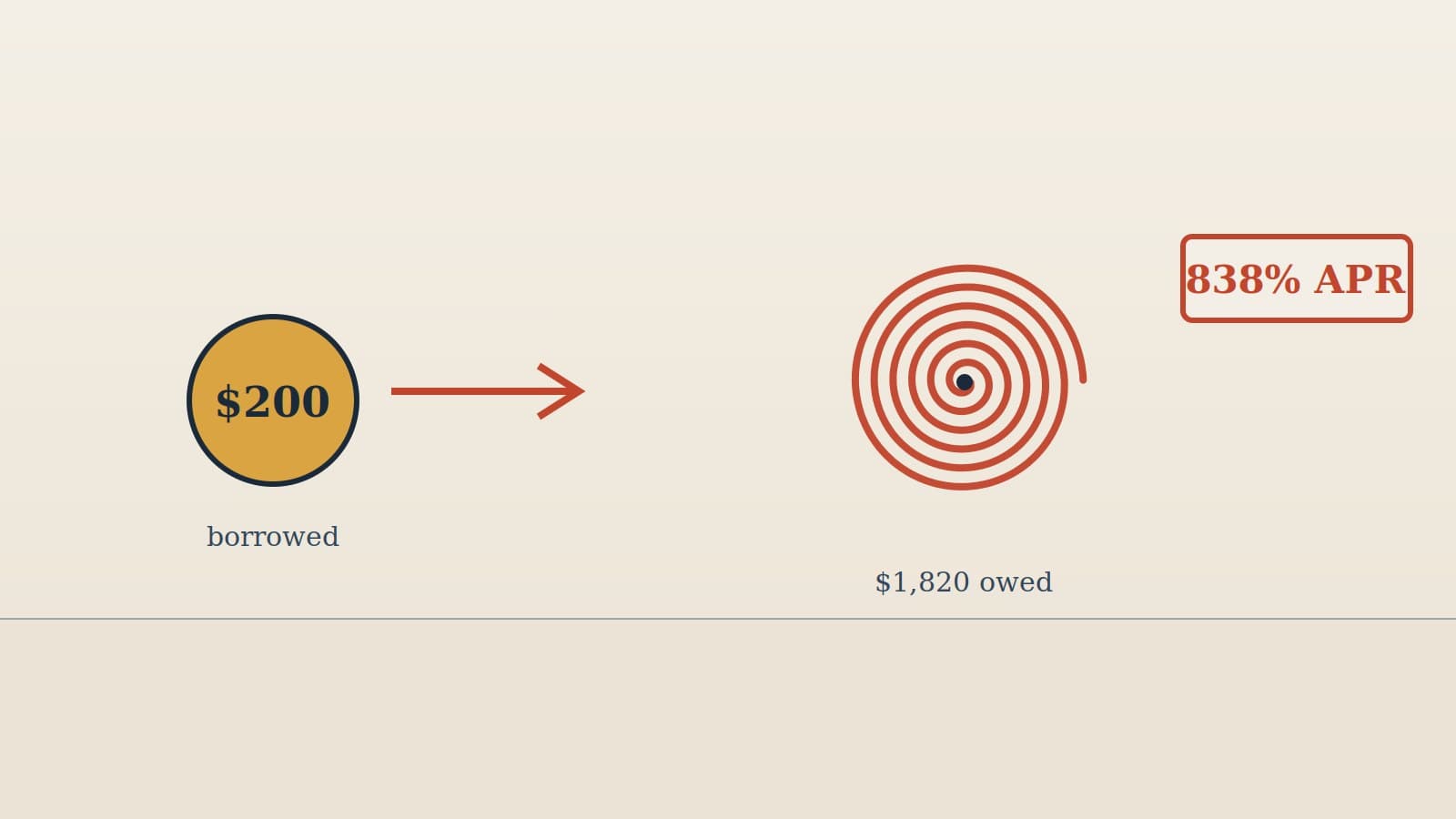

The $200 Loan That Cost $1,820

An 838% payday loan was wiped out entirely — and the lender had to pay her legal bills

What happened

Gloria James worked as a housekeeper at the Hotel DuPont in Wilmington, Delaware, earning roughly 115% of the federal poverty line. She borrowed $200 in cash from National Financial, LLC, a consumer finance company. The entire transaction took about twenty minutes.

The day after taking the loan, James broke her hand cleaning a toilet at work and missed a week of work. When she asked National Financial for any accommodation, the company refused, would not lower her payments, and began collection — calling her workplace and repeatedly trying to debit her prepaid card. After repaying $197, she stopped paying and sued.

The trap in the contract

The loan was structured as a one-year, non-amortizing cash advance with a punishing payment schedule:

- 26 bi-weekly "interest-only" payments of $60 each

- followed by a 27th payment of $60 interest _plus_ the original $200 principal

- Total repayment: $1,820 on a $200 loan — a cost of credit of $1,620

- Stated APR: 838.45% (and on the lender's own planned repayment schedule, closer to 1,095%)

The deception was as important as the math. National Financial trained employees to quote a "block rate" — like "$30 per $100 borrowed" — to make the loan sound like a 30% rate. Employees routinely told customers the APR "had nothing to do with the loan" and was irrelevant unless they kept it outstanding a full year. James focused on the block rate and believed she'd repay about $130 twice and be done. One company witness, asked what price would be too high, would only say he followed state law — and since Delaware caps no interest rates, that effectively meant no price was ever too high.

What the court did

Vice Chancellor Travis Laster of the Delaware Court of Chancery ruled for James on two independent grounds:

- Unconscionability. Applying Delaware's ten-factor unconscionability analysis, the court found the loan both procedurally unconscionable (a financially unsophisticated borrower with no meaningful choice, steered by deceptive "block rate" sales talk) and substantively unconscionable (terms grossly disproportionate to the $200 advanced). The remedy was rescission — the entire loan was unwound.

- Truth in Lending Act (TILA) violation. The court found National had failed to accurately disclose credit terms as federal law requires, which triggered statutory damages plus an award of attorneys' fees and costs to James.

The headline result: the borrower walked away owing nothing further, and the predatory lender had to pay her legal bills.

Why this matters for predatory contracts today

This case is powerful because Delaware has no usury cap, yet the loan still failed. It shows two things:

- "It's legal" is not the same as "it's enforceable." A lender following the letter of a permissive state law can still lose if the bargain is unconscionable.

- Disclosure games have federal consequences. Hiding the true cost of credit behind a "block rate," or telling borrowers the APR doesn't matter, can independently violate the Truth in Lending Act — a federal statute available nationwide.

Red flags to check your own loan for

- A "block rate" or "fee" quoted instead of an APR ("$30 per $100" rather than a clear annual percentage rate).

- Anyone telling you the APR "doesn't matter" or "only counts if you keep it a year."

- Interest-only payments with a balloon — where months of payments never reduce the principal.

- Total repayment that dwarfs the amount borrowed relative to the loan term.

- A lender that refuses any workout and immediately escalates to your employer or bank account.

This article is general legal information, not legal advice. Truth in Lending Act claims and unconscionability standards vary by facts and jurisdiction. If you're trapped in a high-interest loan, consult a licensed attorney or your state's consumer-protection office.